Financials › Fire, Marine And Casualty Insurance

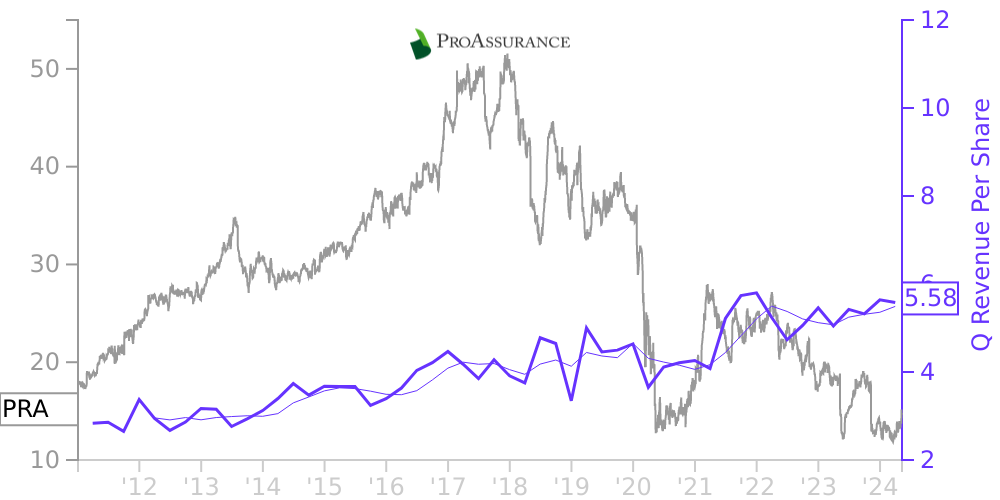

PRA Stock Price Correlated With ProAssurance Financials

External Links ⌄

Income Statement

Cash Flow

Balance Sheet

PRA Income Statement

Enable JavaScript and reload

Revenue, Net:

Cost of Goods & Services Sold:

Gross Profit:

Selling, General & Admin Expense:

Research & Development Expense:

Total Operating Expenses:

Operating Income:

Income Taxes:

Net Income:

PRA Cash Flow

Enable JavaScript and reload

Operating Activities Net Income:

Depreciation, Depletion & Amortization:

Change in Accounts Receiveable:

Net Cash from Operations:

Repurchases/Buybacks Common Stock:

Issuance of Long-term Debt:

Cash Dividends Paid:

Net Cash from Financing Activities:

Property, Plant & Equipment Purchases:

Purchases of Businesses, Net of Cash:

Net Cash from Investing Activities:

Net Change in Cash & Equivalents:

PRA Balance Sheet

Enable JavaScript and reload

Cash and Cash Equivalents:

Short-Term Investments:

Accounts Receivable, Net:

Inventories:

Total Current Assets:

Property, Plant & Equipment, Net:

Total Assets:

Accounts Payable:

Current Portion of Long-Term Debt:

Total Short-Term Liabilities:

Long Term Debt, Non-Current Portion:

Total Long-Term Liabilities:

Total Liabilities:

COMPANY PROFILE

Accounting Policies Organization and Nature of Business

ProAssurance Corporation (ProAssurance, PRA or the Company), a Delaware corporation, is an insurance holding company primarily for wholly owned specialty property and casualty and workers' compensation insurance entities including an entity that provides capital to Syndicate 1729 at Lloyd's. Risks insured are primarily liability risks located within the U.S.

ProAssurance operates in five reportable segments as follows: Specialty P&C, Workers' Compensation Insurance, Segregated Portfolio Cell Reinsurance, Lloyd's Syndicates and Corporate. For more information on the Company's segment reporting, including the nature of products and services provided and financial information by segment, refer to Note 18.

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of ProAssurance Corporation, its wholly owned subsidiaries and VIEs in which ProAssurance is the primary beneficiary. See Note 16 for more information on ProAssurance's VIE interests. Investments in entities where ProAssurance holds a greater than minor interest but does not hold a controlling interest are accounted for using the equity method. All significant intercompany accounts and transactions are eliminated in consolidation. ProAssurance subsidiaries located in the U.K. are normally reported on a quarter lag due to timing issues regarding the availability of information, except when information is available that is material to the current period. Furthermore, investment results associated with ProAssurance's FAL investments and certain U.S. paid administrative expenses are reported concurrently as that information is available on an earlier time frame.

Reclassifications

Certain insignificant prior year amounts have been reclassified to conform to the current year presentation.

Basis of Presentation

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, revenues and expenses, and disclosures related to these amounts at the date of the financial statements.

Accounting Policies

The significant accounting policies followed by ProAssurance in making estimates that materially affect financial reporting are summarized in these Notes to Consolidated Financial Statements. The Company evaluates these estimates and assumptions on an ongoing basis based on current and historical developments, market conditions, industry trends and other information that the Company believes to be reasonable under the circumstances, including the potential impacts of the COVID-19 pandemic (see "Item 1A, Risk Factors" included in this report for additional information). The Company can make no assurance that actual results will conform to its estimates and assumptions; reported results of operations may be materially affected by changes in these estimates and assumptions.

Recognition of Revenues

Insurance premiums are recognized as revenues pro rata over the terms of the policies, which are principally one year in duration.

Losses and Loss Adjustment Expenses

ProAssurance establishes its reserve for losses and LAE ("reserve for losses" or "reserve") based on estimates of the future amounts necessary to pay claims and expenses associated with the investigation and settlement of claims. The reserve for losses is determined on the basis of individual claims and payments thereon as well as actuarially determined estimates of future losses based on past loss experience, available industry data and projections as to future claims frequency, severity, inflationary trends, judicial trends, legislative changes and settlement patterns.

Management establishes the reserve for losses after taking into consideration a variety of factors including premium rates, historical paid and incurred loss development trends, and management's evaluation of the current loss environment inclu

ProAssurance Corporation (ProAssurance, PRA or the Company), a Delaware corporation, is an insurance holding company primarily for wholly owned specialty property and casualty and workers' compensation insurance entities including an entity that provides capital to Syndicate 1729 at Lloyd's. Risks insured are primarily liability risks located within the U.S.

ProAssurance operates in five reportable segments as follows: Specialty P&C, Workers' Compensation Insurance, Segregated Portfolio Cell Reinsurance, Lloyd's Syndicates and Corporate. For more information on the Company's segment reporting, including the nature of products and services provided and financial information by segment, refer to Note 18.

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of ProAssurance Corporation, its wholly owned subsidiaries and VIEs in which ProAssurance is the primary beneficiary. See Note 16 for more information on ProAssurance's VIE interests. Investments in entities where ProAssurance holds a greater than minor interest but does not hold a controlling interest are accounted for using the equity method. All significant intercompany accounts and transactions are eliminated in consolidation. ProAssurance subsidiaries located in the U.K. are normally reported on a quarter lag due to timing issues regarding the availability of information, except when information is available that is material to the current period. Furthermore, investment results associated with ProAssurance's FAL investments and certain U.S. paid administrative expenses are reported concurrently as that information is available on an earlier time frame.

Reclassifications

Certain insignificant prior year amounts have been reclassified to conform to the current year presentation.

Basis of Presentation

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, revenues and expenses, and disclosures related to these amounts at the date of the financial statements.

Accounting Policies

The significant accounting policies followed by ProAssurance in making estimates that materially affect financial reporting are summarized in these Notes to Consolidated Financial Statements. The Company evaluates these estimates and assumptions on an ongoing basis based on current and historical developments, market conditions, industry trends and other information that the Company believes to be reasonable under the circumstances, including the potential impacts of the COVID-19 pandemic (see "Item 1A, Risk Factors" included in this report for additional information). The Company can make no assurance that actual results will conform to its estimates and assumptions; reported results of operations may be materially affected by changes in these estimates and assumptions.

Recognition of Revenues

Insurance premiums are recognized as revenues pro rata over the terms of the policies, which are principally one year in duration.

Losses and Loss Adjustment Expenses

ProAssurance establishes its reserve for losses and LAE ("reserve for losses" or "reserve") based on estimates of the future amounts necessary to pay claims and expenses associated with the investigation and settlement of claims. The reserve for losses is determined on the basis of individual claims and payments thereon as well as actuarially determined estimates of future losses based on past loss experience, available industry data and projections as to future claims frequency, severity, inflationary trends, judicial trends, legislative changes and settlement patterns.

Management establishes the reserve for losses after taking into consideration a variety of factors including premium rates, historical paid and incurred loss development trends, and management's evaluation of the current loss environment inclu

Free historical financial statements for ProAssurance Corp.. See how revenue, income, cash flow, and balance sheet financials have changed over 61 quarters since 2011. Compare with PRA stock chart to see long term trends.

Data imported from ProAssurance Corp. SEC filings. Check original filings before making any investment decision.