Materials › Metal Cans

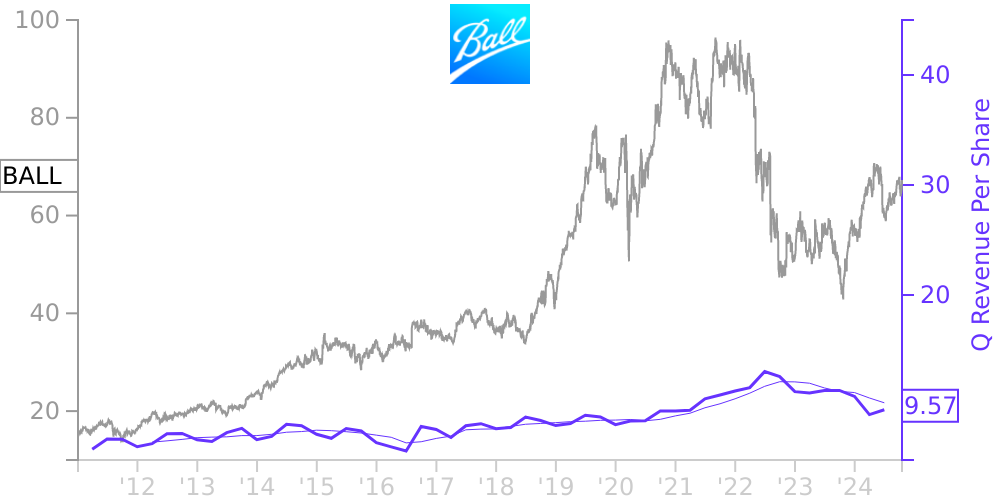

BALL Stock Price Correlated With Ball Financials

External Links ⌄

Income Statement

Cash Flow

Balance Sheet

BALL Income Statement

Enable JavaScript and reload

Revenue, Net:

Cost of Goods & Services Sold:

Gross Profit:

Selling, General & Admin Expense:

Research & Development Expense:

Total Operating Expenses:

Operating Income:

Income Taxes:

Net Income:

BALL Cash Flow

Enable JavaScript and reload

Operating Activities Net Income:

Depreciation, Depletion & Amortization:

Change in Accounts Receiveable:

Net Cash from Operations:

Repurchases/Buybacks Common Stock:

Issuance of Long-term Debt:

Cash Dividends Paid:

Net Cash from Financing Activities:

Property, Plant & Equipment Purchases:

Purchases of Businesses, Net of Cash:

Net Cash from Investing Activities:

Net Change in Cash & Equivalents:

BALL Balance Sheet

Enable JavaScript and reload

Cash and Cash Equivalents:

Short-Term Investments:

Accounts Receivable, Net:

Inventories:

Total Current Assets:

Property, Plant & Equipment, Net:

Total Assets:

Accounts Payable:

Current Portion of Long-Term Debt:

Total Short-Term Liabilities:

Long Term Debt, Non-Current Portion:

Total Long-Term Liabilities:

Total Liabilities:

COMPANY PROFILE

1. Critical and Significant Accounting Policies The preparation of Ball Corporation’s (collectively, Ball, the company, we or our) consolidated financial statements in conformity with accounting principles generally accepted in the United States of America (U.S. GAAP) requires Ball’s management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent liabilities at the date of the financial statements and reported amounts of revenues and expenses during the reporting periods. These estimates are based on historical experience and various assumptions believed to be reasonable under the circumstances. Ball’s management evaluates these estimates on an ongoing basis and adjusts or revises the estimates as circumstances change. As future events and their impacts cannot be determined with precision, actual results may differ from these estimates. In the opinion of management, the financial statements reflect all adjustments necessary to fairly present the results of the periods presented. Critical Accounting Policies The company considers certain accounting policies to be critical, as their application requires management’s judgment about the impacts of matters that are inherently uncertain. Detailed below is a discussion of the accounting policies that management considers to be critical to the company’s consolidated financial statements. Revenue Recognition in the Aerospace Segment Sales under fixed-price long-term contracts in the aerospace segment are primarily recognized using percentage-of-completion accounting under the cost-to-cost method. At contract inception, the company assesses the goods and services promised in its contracts with customers and identifies a performance obligation for each promise to transfer goods or services to the customer. The performance obligation may be represented by a good or service (or a series of goods or services) that is distinct, or by a series of distinct goods or services that are substantially the same and have the same pattern of transfer to the customer. In each of these scenarios, the company treats the promise to transfer the customer goods or services as a single performance obligation. Backlog represents the estimated transaction prices on performance obligations to customers for which work remains to be performed. To identify its performance obligations, the company considers all of the goods or services promised in the contract, regardless of whether they are explicitly stated or are implied by customary business practices. The company has determined that the following distinct goods and services represent separate performance obligations: ● Manufacture and delivery of distinct spacecraft and/or hardware components; ● Research reports, for contracts where such reports are the sole or primary deliverable; ● Design, add-on or special studies for contracts where such studies have stand-alone value or a material right exists due to discounted pricing; and ● Warranty and performance guarantees beyond standard repair/replacement. Performance obligations with no alternative use are recognized over time, when the company has an enforceable right to payment for efforts completed to-date. Because of sales contract payment schedules, limitations on funding, and contract terms, the company’s sales and accounts receivable generally include amounts that have been earned but not yet billed. The company’s payment terms vary by the type and location of the company’s customer and the products or services offered. All payment terms are less than one year. Contracts are often modified to account for changes in contract specifications and requirements. The company considers contract modifications to exist when the modification either creates new or revised enforceable rights and obligations. Most of the company’s contract modifications are for goods or services that are not distinct from the existing contract due

Free historical financial statements for Ball Corp. See how revenue, income, cash flow, and balance sheet financials have changed over 61 quarters since 2011. Compare with BALL stock chart to see long term trends.

Data imported from Ball Corp SEC filings. Check original filings before making any investment decision.